How to Improve your Credit Score

A good credit score can enhance various aspects of your financial life. Not only can a solid credit score make things easier for receiving loan approvals and lower interest rates, but you can often access better credit card offers with rewards and even lower insurance premiums that can help you save a significant amount of money over time.4 5

A credit score can also impact housing and some employment opportunities that use your credit history to determine your ability to be responsible with your debt obligations. If you're currently in a bad credit position, you may wonder how to improve your credit score effectively to reap the benefits of a higher credit standing that can give you financial stability and achieve your desired goals.

While raising your credit score can seem difficult and overwhelming, many strategies have proven to be useful for raising a credit score over time. Regardless of the credit rating you're looking to accomplish, you can expect to put your credit history in a positive position by executing the following credit-building methods:

- Pay All of Your Bills on Time on Their Scheduled Due Dates

- Monitor Your Credit Report Frequently to Dispute Any Errors and Check for Unpaid Balances

- Keep Your Overall Credit Utilization Ratio Low By Controlling Your Spending and Paying Off Your Balance

- Limit the Number of Times You Apply for New Credit

- Maintain Your Old Accounts Open to Extend the Length of Your Credit History

- Have a Diverse Credit Mix to Show Lenders You Can Manage Different Financial Commitments Responsibly

Increasing your credit score can be straightforward if you focus on practicing healthy financial habits and ensuring your credit reports are accurate. If you miss payments or apply for several credit card accounts simultaneously, for example, you can negatively impact your credit history and affect your chances of achieving some of the financial goals you have in mind. If you start working on boosting your credit, you should check for any mistakes on your credit report that can severely harm your score. You can raise your credit score over time if you successfully dispute any inaccuracies and the credit bureau fixes or removes them from your credit file. Take advantage of Max Cash®'s exclusive offers to discover your credit score and conveniently monitor your credit report. 2

CreditScoreiQ

Key Features

- Comprehensive Credit Report Access: View Experian, Equifax, and TransUnion scores.

- DIY Dispute Tools for Errors: Identify and challenge negative report items.

- Credit Monitoring with Change Alerts: Receive notifications for report updates.

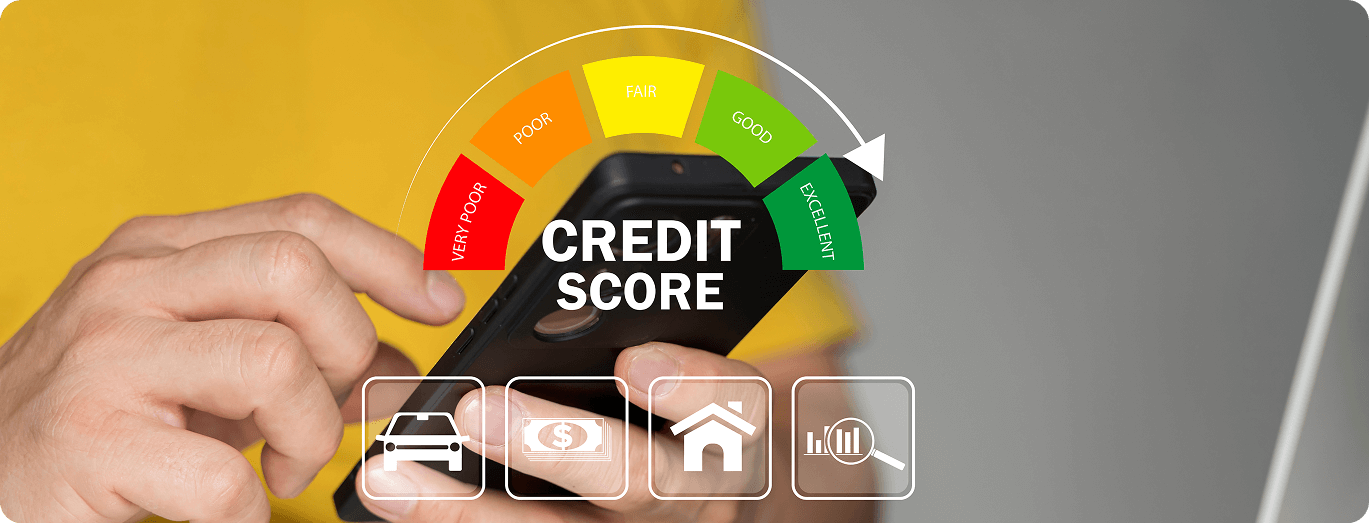

What is a Credit Score and How is it Calculated?

Before you start working on improving your credit score, you should understand what a credit score is and what factors the three major credit bureaus follow to come up with your rating. Essentially, a credit score is a three-digit number (usually from 300 to 850) that estimates your creditworthiness, which lenders, insurance companies, and even some landlords use to review your credit profile. If you plan to apply for an unsecured loan, your credit score can significantly influence the interest rate you'll access once you start paying back your loan. If you have poor credit, a lender may charge you higher interest rates that can make the repayment process expensive and challenging to afford. 4 5

Keep in mind that there are various credit scoring models available, but the two main systems that financial institutions often use to assess an individual's credit risk are the FICO® and VantageScore® systems. Although both models are widely used by banks, lenders, and credit card issuers across the United States, you can expect an entity to use the FICO® score system to establish your creditworthiness and determine your approval for different things, such as loans, new credit cards, housing, and insurance premiums. When it comes to your FICO® credit score, the Fair Isaac Corporation (FICO® ) will use several characteristics shown on your credit report to calculate your rating. If you want to boost your credit score, it is advised that you focus on the key factors in your credit file to see it improve over time.

Take a look at the different elements that FICO® takes from your credit report to calculate your credit score:

- Your Payment History

- The Total Amount You Owe

- The Length of Your Credit History

- Your Credit Mix

- New Credit Applications

If you don't know what your current credit score is, you can easily access that data through multiple online sources, including free services from the three major credit bureaus, free credit score websites, or by going to your bank / credit card issuer's digital platforms. In the event that you need help assessing your credit score information, you can also opt to speak with a nonprofit credit or housing counselor to check your credit score without spending any money. It's worth noting that you can also view your credit data online by working with Max Cash®'s aforementioned offers to easily see your credit score from the comfort of your home.2 Whichever method you choose to review your credit, you can determine what your present credit position is, so you can start boosting your credit score immediately towards your desired goal.

Dial 833-207-9052 if you have questions about credit scores and the different factors that make up your rating. If you want to increase your chances of getting approved for one of the many loans you can get with the help of Max Cash®, you can simply implement the previously mentioned strategies to put your credit score in a stronger position.2 5

What Increases Your Credit Score Faster?

If you're thinking about getting a loan just to pay bills or cover an unexpected expense, you may be considering improving your credit score quickly to increase your chances of getting funded.5 You may not have enough time to gradually grow your credit score before you apply for the loan you need to recover financially, so you may be searching for other tips to increase your credit rating faster. While it's challenging to boost your credit score instantly, you can still find some effective ways to positively influence your score fast if you follow some successful techniques. If you've taken the right measures to change your financial habits and execute the best credit-building strategies, you may see an improvement in your credit score as soon as 30 to 45 days.

Check out some of the most efficient methods you can use to increase your credit score quickly when you need it in a favorable position prior to a loan application:

- Use a Secured Credit Card to Establish Positive Credit Habits and Build Your Credit Score

- Request an Increase on Your Credit Limit to Lower Your Credit Utilization Ratio Quickly

- Pay Down Your Credit Card Debt Before Your Billing Cycle to Raise Your Score

- Become an Authorized User on a Primary Cardholder's Well-Managed Credit Card Account to Benefit From Their Positive Credit History

It's worth mentioning that the timeline to improve your credit score can vary depending on your financial situation and your unique objectives. If you want to change your credit score from "Fair" to "Good," it might not take as much time to see it grow compared to changing it from "Poor" to an "Excellent" score. Individuals with late or missed payments may have a derogatory mark on their credit reports that typically lasts up to 7 years. If you only have one late payment, though, you may have a quicker process to increase your credit score compared to more challenging situations, such as Chapter 7 bankruptcies, which can take up to 10 years to clear from your file.

Regardless of what your current circumstances are, you can see an improvement in your credit score if you execute the appropriate strategies and follow the correct habits that positively impact your financial history. Although your desired changes may not be as quick as you might have hoped, you can still see a positive growth in your credit standing if you put some time and effort on your part. If you need money now to cover a sudden expense, you don't have to wait to boost your credit score to get your emergency cash. You can simply apply for secured loans, like auto title loans, to get the funds you need to regain a stable financial position, even if you have a bad credit score. 5

CreditScoreiQ

Key Features

- Comprehensive Credit Report Access: View Experian, Equifax, and TransUnion scores.

- DIY Dispute Tools for Errors: Identify and challenge negative report items.

- Credit Monitoring with Change Alerts: Receive notifications for report updates.

What is the 15-3 Credit Card Trick?

You might have heard of the popular "15-3 credit card trick" during your search for the fastest ways to boost your credit score. If you want to improve your credit rating in a short amount of time, you may be considering using that strategy to put yourself in a better position to qualify for loans or accomplish other objectives. However, you must understand how this technique works before you decide to implement it into your credit-building system. The "15-3 credit card trick" is basically a financial "hack" that suggests you pay your credit card bill in two installment payments: one payment about 15 days before your due date, and the other payment 3 days before the due date.

The purpose of the "15-3 credit card trick" is to increase the number of on-time payment entries your credit card issuer will report to the major credit bureaus when you make two separate payments consecutively. Many people think that splitting their bill with timely payments will improve their credit scores significantly and fast, but the "15-3 Rule" isn't the magic method they believe it to be. While making multiple payments can help you lower your credit utilization ratio, you may not increase your credit score that much if you divide your bill into two payments each month. Typically, credit card issuers report your payment activity once a month, so if you make two on-time payments within the "15-3" timeframe, your account may show up as "current" on your credit report, with no changes in the state of your account.

What you can do instead of the "15-3 credit card trick" is to pay off your credit card balance prior to your issuer's reporting date, rather than waiting for your scheduled due date. Since most credit card issuers report your account status around your statement closing date and not your payment due date, you can potentially boost your credit score if you make a timely payment before they make that report. It's worth noting that credit card billing periods are usually 28 to 31 days, with the final day being your statement closing date. If you pay back your credit card 15 or 3 days before your billing due date and after your statement closing date, you may not see any impact on the balance that the issuer reports to the major credit bureau.

If you want to raise your credit score quickly, you can follow the aforementioned tips to put your credit where you want it to be. Don't forget that it takes time and effort to boost your credit rating, but you may find it more effective to increase your score through those reliable methods instead of using the "15-3 credit card trick." Take advantage of those proven techniques now to improve your credit score in a position that can give you some leverage in many financial decisions.

Frequently Asked Questions About

Improving Your Credit Score

Below are answers to some of the most frequently asked questions about improving your credit score to good standing:

Increasing your credit score by 200 points in such a short amount of time is typically not realistic. However, it is possible to improve your score within 6 months to a year, depending heavily on how many negative factors you have in your credit report and how quickly they can be addressed. Make sure to follow high-impact methods to boost your credit rating fast, such as lowering your credit utilization ratio by paying down credit card balances, disputing errors on your credit files immediately, paying all of your bills on time, and becoming an authorized user on a trusted account.

Although many credit-building tips use credit cards to achieve this financial goal, you can actually find other methods to improve your credit score if you aren't a cardholder. Regardless of the reasons you don't own a credit card, you can effectively boost your credit score without one when you implement the following strategies:

- Take Out a Credit-Builder Loan to Demonstrate a Positive Financial History

- Pay Off Your Current Debt By Making Timely Payments Each Month

- Become an Authorized User on a Reliable Family Member's Account

- Get Credit for Rent or Utility Bill Payments Through a Third-Party Service

- Apply for a Loan with a Co-Signer to Increase Your Approval Odds and Establish a Responsible Payment History

Restoring your credit rating can take a few months for minor issues to a year or more for significant problems, with major events, like bankruptcy and vehicle repossession, lingering for 7 to 10 years on your credit report. While it's difficult to pinpoint the exact timeline you can expect to fix your credit score, you can see some improvements in your credit position if you have positive financial habits, like making on-time payments on your debts and keeping your credit utilization rate low.

More Credit Score Resources

How to Check You Credit Score?

Many experts recommend checking your credit score once per year at the very least. Learn how to connect to your credit rating online with the help of Max Cash®!

How to Monitor Your Credit?

Monitoring your credit score is an important part of preventing fraud and improving your financial health. Discover online monitoring options with the help of Max Cash®!

How to Improve Your Credit Score?

Worried about your credit affecting your chances for loan approval? Learn how to improve your credit score with proven strategies today!

How to Build Credit?

Build your credit score with proven strategies like on-time payments, low balances, credit monitoring, and smart tools to improve your financial future.